Services

CREDIT REFERENCING & SCORE CARDING

A Thoroughly “Synapsed Referencing” is translated into a “Scoring Card” Mechanism

These Derived Metrics (via RATIO and other Para Legal Analysis) are then aggregated to a Profile CREDIT Score

The Score is indicative of a Assigned CREDIT – in TENOR and VALUE

The VALUE is DRILLED down into GREEN, YELLOW and RED Timelines for ascertaining CREDIT DICIPLINE / DELINQUENCY

COLLECTIONs Management - Both DOMESTIC & INTERNATIONAL

When we have a Good Process in place for Knowing our Customers / Clients then we generally tend to have a Manageable A.R ::

Yet, with Growing Business Needs, we might have to relax the CREDIT POLICY

With this Relaxation Comes an Additional INPUT of “A.R Surveillance”

A.R Surveillance should be @ Regular Periods with ALL STAKEHOLDERs

DICIPILNE in ToP has to be Maintained to ensure a LEAN A.R

Risk Mitigation via TRADE CREDIT INSURANCE

Today; in most Enterprises the “Bad Debts” written off / The charge on P&L ranges anywhere between 2% to 4% of Gross Turnover

Taking up a TRADE CREDIT Insurance; covers this LOSS; and this for just 0.40% of Turnover!

The Cash Flows will improve as we don’t have the debt to get delinquent and these debts can be converted very early on in the Collection Cycle by Banking TOOL of :: FACTORING

The added advantage is that the insurance company will have a detailed credit assessment done on the prospective customer and the credit risk will be in lines with the market dynamics

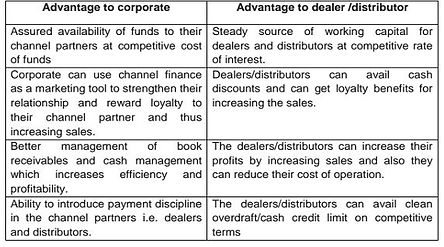

Collection & BANKING Tools - CHANNEL FINANCING

MIS Dash Boards for the CXO Suite

Revolving DSO (7 Customised / Relevant Methods)

Collections and DSO TARGET Monitoring – Intra Day

CCC

Collections Efficiency

Contribution Levels

BUDGET Based Collections Target Setting and INTRA DAY Monitoring

BAD DEBTs and CHARGE Monitoring

PRE BID TENDERs :: Status and ON GOING TENDERs – Status – C/F Position

TREASURY Reports :: FOREX – Contracts (Exposure and Covers / HEDGEs)

WORKING CAPITAL :: DAY SCOREs

TRAINING - "CASH before YOU CRACK"

Reading and Interpretation of Financial Statements

Understanding Ratios and Interpreting them

The Importance and Criticality of TENDER Vetting and TERM SHEETING

PROS and CONS of KYC, Customer Profiling, CREDIT Limits Setting

Collections Techniques and Best Practices

Financial Discipline and Effective Communication

Dunning Systems

How to get DEBTs Insured and Factored

Excel and MS Projects as a Tool to MAP Time Lines with Billing Mile Stones

Negotiating a TOUGH and IRATE Customer and getting our STUCK Payments from them

LEGAL Coursing

Prospective Client / CUSTOMER PROFILING

Complete KYC Induction of the Prospective Customer via an Evolved-Evolving Template.

Face to Face Interaction with the Prospect

Trade Reference and Market Information on the Prospect,

Historical Business / Financial / Legal TRAIL

Visit @ the Prospective Customer’s Premises

Prospect’s Bankers Reference

TENDER VETTING & Term Sheeting

A Tender is a Prospective Contract in the DRAFT Mode

A Tender Carries - Commercial, TAX, PRICE and Profit Implications

A Tender is usually Biased to Safe Guard the Customer’s interests via this DRAFT Tender Contract

WE have to RIP (Read in Particular) the Tender; to Ascertain the Areas that pose FINANCIAL and TECHNICAL RISKs / Disadvantages / Threats to us whilst we Execute this Prospective Tender

These RISKs needs to be Tabulated and shared with the TENDER COMMITTEE for its Deliberation and Authorization as per LoA

RISK MITIGATION Techniques, Tools and Processes needs to be implemented as a HEDGE

All Complex Tenders, FIDIC Tenders, Large Government Tenders come with Multiple Legal, Financial and Engineering Clauses that bear great implication on the Cost of the Project and the Profit Margin at the end of the Project

Particularly when the Project is spread across Multiple Years and there are Imported Raw Materials involved which has bearing on the Exchange Gain / Loss on Foreign Currency

The Appropriate Mile Stone Billing with Proportionate BoM

Dunning on Running Bills (R/A Bills)

Compliance on Tender Requirements – Highlights and Monitoring

PROTRACTED A.R Collections - Both Domestic and International

Our Standard Premise being - ALL Debts are Collectable

We interact with the Customer and Understand the Basic Reason for their Delay in Payment

We Correct our Mistakes (if there are) or Resolve Issues that pertain to our LACK

We Engage the DECISION Makers (CxOs) @ the Customer for Quick Release of Payments

We Educate the Customer on Betterment of their WC Management

We Constantly Engage the Customer via IT Tools for them to be aware of the LEGAL implications of not having paid the DEBT on Time

We have interacted with 3,000 + Protracted Customers and have had almost 100% Success Rate

We ensure that the Best Practices of Credit Management is employed through Appropriate Credit Policy, SoP and Procedures so that PROTRACTED DEBTs are a HISTORY!

Collection & BANKING Tools – FACTORING

There are various banks today in India offering this product

The Banks provide funding upto 90% of the invoice value

The client may have to sign an agreement with the bank were the unpaid debts get subrogated to the bank post the credit period

The prevailing rate is 10%

This rate will go down as much as 8.50 % if our debts are insured

In case the debts are insured the factoring is done without recourse.

Collection & BANKING Tools - E- Payment Gateway/s

The BANK’s Server vide its Software is Synchronized with our AR & AP LEDGERs

Virtual and Unique ERP Customer Codes are Generated

The Gateway Reference is shared with the Customer

The LEDGER (Open Items) is available for the Customer to Review and Pay

Once the Identified & Selected OPEN ITEMS are Paid…ONLINE

The Bank Server Uploads these payments as Receipts into our ERP (SAP)

The Auto Run ADF ensures Cash Application is done without human intervention

Thereby, Reducing the Possibility for LEDGER errors, RECONCILATIONs & Excuses for delayed payments…

LEGAL Engagement for DELINQUENCY Mgmt. (Dom. & Overseas)

Delinquency Management ::

Cheque Bouncing (Return) under Sec 138 of the Negotiable Instruments Act

Summary Suits

Winding Up Petition

Out of Court Settlements

Insurance Claims